-

June 08, 2026

- |

- |

-

Categories: Blogs

Technology markets are entering a new phase of transformation, forcing vendors and partners to rethink where value is created and how relevance is sustained.

Last week, while recording a podcast with a group in Europe, the host and I started lamenting the terms that were once hot in the tech industry and channel but are no longer used with much frequency.

Honestly, I can’t remember the last time I uttered the words “Big Data” or “Internet of Things.” We rarely hear people talk about mobility or blockchain as the big waves influencing everything. While cloud computing remains part of the daily lexicon, it’s more or less the foundation on which other things are built.

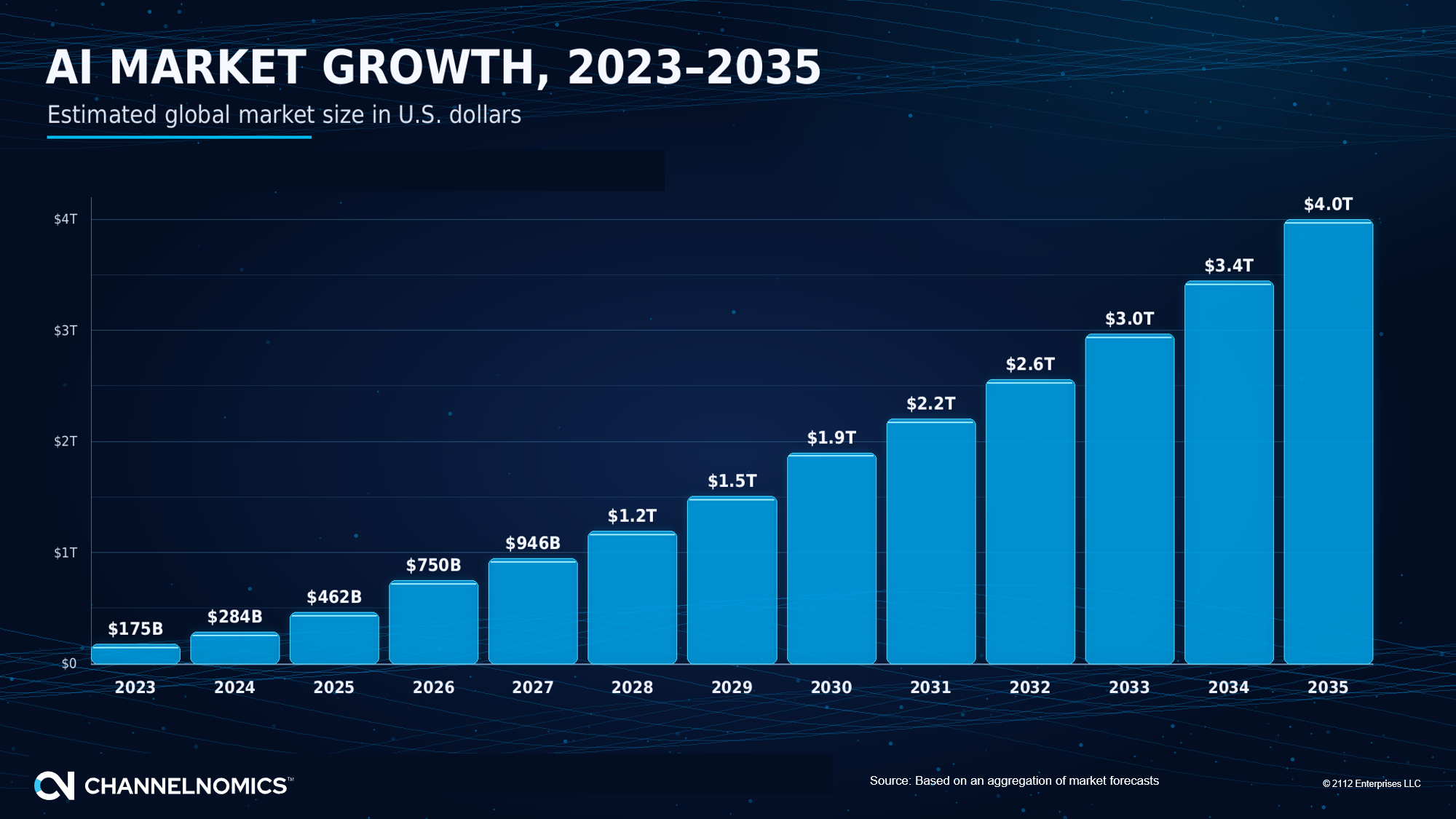

Today, it’s all about artificial intelligence. And with good reason. The technology is still nascent, yet growing fast. In 2023, when chatbots went mainstream, the global AI market was valued at around $175 billion. Today, depending on the estimate, it’s somewhere between $600 billion and $900 billion. By 2030, it will likely fall somewhere between $1.8 trillion and $2 trillion. By 2035, it could approach $4 trillion.

These are remarkable figures, especially given that the global IT market generates roughly $6 trillion in annual spending.

Yet AI isn’t the only driving force. AI is reshaping the broader global technology market and channel. It’s changing customers’ needs and expectations. It’s compelling vendors and channel partners to adjust their business models and value propositions to ride this wave and remain relevant in the market. And market relevance equates to long-term viability.

While I bristle at saying that “this is the greatest transformational period ever,” as was said about cloud computing, IoT, and Big Data before, the current breadth and pace of change are undeniably remarkable.

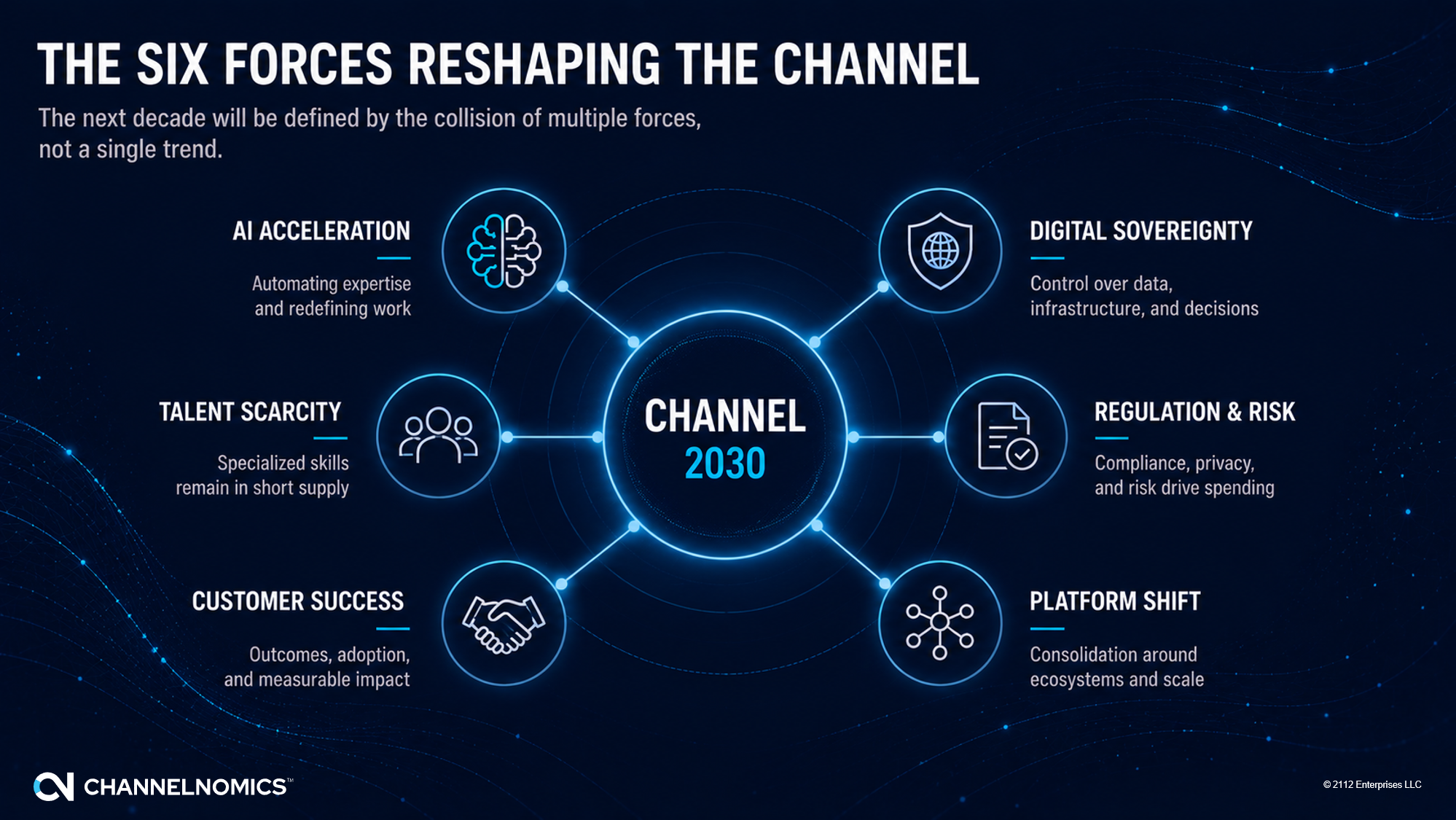

Channelnomics asked hundreds of solution providers — resellers, integrators, managed service providers, aggregators, and professional services consultants — about the forces impacting their thinking and future planning. The results point to six forces reshaping the channel. These are the true drivers of channel evolution and adaptation to future market conditions.

- AI Acceleration: The rapid integration of artificial intelligence into business operations, products, and services. AI is automating routine tasks, augmenting decision-making, creating new business models, and changing how work is performed. For channel partners, AI represents both a growth opportunity and a disruptive force that will redefine value creation.

- Talent Scarcity: The persistent shortage of skilled technical, sales, cybersecurity, data, and AI professionals. As technology becomes more complex, organizations struggle to recruit, develop, and retain qualified talent. This scarcity increases the value of automation, managed services, training, and specialized expertise.

- Customer Success: The shift from selling products and projects to delivering measurable business outcomes. Customers increasingly evaluate suppliers based on adoption, utilization, productivity gains, risk reduction, and return on investment rather than features alone. Success is defined by ongoing customer value rather than the initial transaction.

- Digital Sovereignty: The growing demand for control over data, infrastructure, applications, and digital operations. Governments and enterprises are increasingly concerned with data residency, security, resilience, regulatory compliance, and reducing dependence on external providers. This trend is reshaping cloud, cybersecurity, and infrastructure investment decisions.

- Regulation & Risk: The expanding influence of compliance requirements, cybersecurity threats, privacy regulations, geopolitical uncertainty, and operational risk. Organizations are investing more heavily in technologies and services that improve security, governance, resilience, and regulatory compliance. Risk management is becoming a primary driver of technology spending.

- Platform Shift: The movement away from fragmented point solutions toward integrated platforms and ecosystems. Organizations seek to simplify operations, improve interoperability, reduce complexity, and gain better visibility across their environments. As platforms become central to technology strategies, partners must increasingly build capabilities around ecosystems rather than individual products.

AI is a catalyst for change, but it’s also bringing other issues to the fore that vendors and their partners must consider in their strategic planning and business development. Talent, customer success, sovereignty, regulation, risk, and platforms aren’t secondary concerns. They're the conditions under which AI adoption, technology investment, and channel transformation will unfold.

The thing about these influencing forces is that they point to one common denominator: expertise and experience.

As AI reshapes everything, it will also change the nature of value in technology. It’s becoming clearer that product sales are not the root of the value delivered to end customers through partners. Rather, the value lies in knowing what to do with technology, how to apply it, and when to act.

For vendors, this means reshaping channel programs around what partners do for their customers rather than chasing traditional land-and-expand models. It means caring as much about inputs and outcomes as the products being sold.

For channel partners, the future is clear. It’s about trading on knowledge rather than products and services. Offerings are how value is created and delivered, but customers will truly need expertise and know-how. This will require resetting engagement models to focus on impact rather than point-in-time sales.

The future is already here. AI has set the wheels of change in motion. The choice going forward is whether to move with that change or get caught beneath it.

*********************************************************************************

Larry Walsh is the CEO, chief analyst, and founder of Channelnomics. He’s an expert on the development and execution of channel programs, disruptive sales models, and growth strategies for companies worldwide.

Unauthorized sales through bad actors in the channel plague vendors partner programs and undermine ...

There’s more trouble in sight for the tech space, but vendors remain confident in partners’ ability ...

Channelnomics iQ Exclusive An in-depth explanation of how partners profit from and monetize ...