Vendors are experiencing slow and longer sales cycles in the channel despite partner confidence in growth. Why the contradiction?

At Channelnomics, we field questions about best practices, partner strategies, and channel programs every day. In the “Ask Channelnomics” series, we answer some of the questions we receive most from vendors.

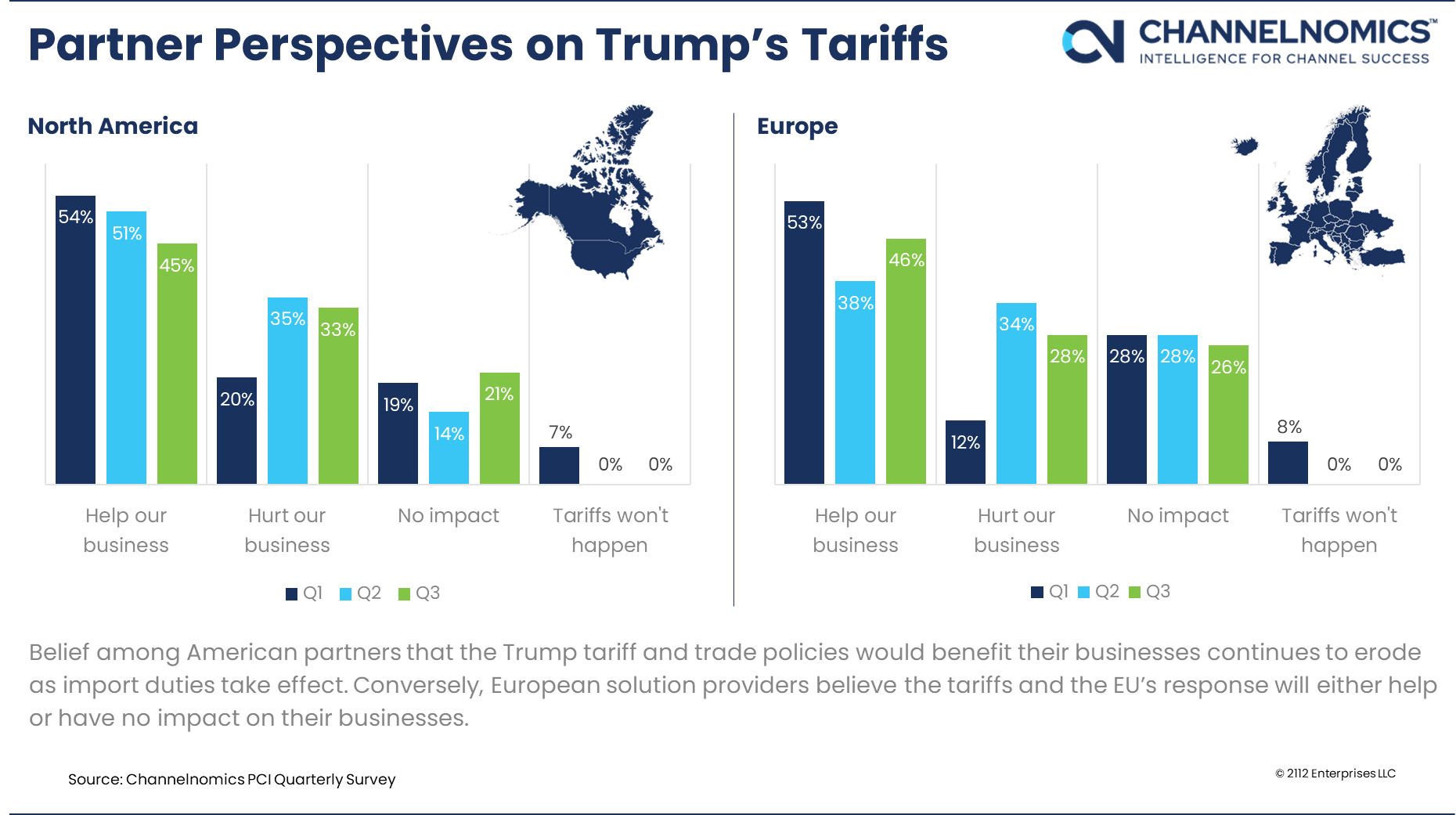

Question: According to Channelnomics, partner confidence remains strong despite global economic uncertainty. Yet we’re seeing sluggish partner sales, longer sales cycles, and lower average deal sizes. What’s going on?

Answer: The contradiction is real and observable. Partner confidence and business development plans remain relatively high. While economists warn that the Trump administration’s tariffs and trade policies could disrupt global commerce, the U.S. economy remains relatively stable. Unemployment is steady, inflation is declining, GDP forecasts are being revised upward, and import duties are filling federal coffers without yet showing up in product pricing. Why the contradiction?

Well, it’s complicated.

The business community largely anticipated that Trump would reintroduce tariffs in his second term. Tariffs were central to his 2024 campaign. Even before the administration implemented global tariffs in April, technology and manufacturing firms began stockpiling materials and finished goods to avoid import duties. The 90-day pause — later extended by another 30 days — created additional room to build low-cost inventory reserves.

Many tariffs haven’t yet taken effect, and businesses are working through stocked inventory. This has helped keep prices stable. Exporters affected by new tariffs are lowering wholesale prices to reduce the burden on importers. Many importers, in turn, are absorbing added costs by compressing profit margins.

Still, this doesn’t fully explain why confidence is high while sales performance is weak. Vendors and partners report that sales cycles have grown longer because of economic uncertainty. Organizations across the spectrum — from SMBs to enterprises — are cutting costs to offset rising operational expenses and brace for expected price increases once tariffs take full effect. Global growth continues, but it’s uneven across geographies and sectors. Much of the revenue growth reported by tech vendors is due to price increases, not unit expansion.

Partners also say more stakeholders are now involved in purchasing decisions, extending the review process. Demand for proofs of concept and trialware is rising. And when deals do close, they’re often smaller than forecasted.

This pattern is consistent across the channel, regardless of technology category, customer segment, or vertical focus. One notable exception is the U.S. public sector, where the Trump administration’s aggressive cancellation of channel-based contracts is hitting resellers and service providers especially hard.

Another dynamic that Channelnomics is hearing about anecdotally is the presence of “trapped budgets.” Many enterprises have earmarked funds for artificial intelligence projects, often reallocating dollars from conventional IT products and services. These deferrals limit short-term spending across other technology categories.

All of this must be seen in context. Expectations for 2025 were already high relative to underlying market conditions. Partners continue to project revenue and profit gains of 10% to 14%, and vendors report similar outlooks for indirect revenue. Meanwhile, analyst firms forecast global IT market growth of 9% to 11%. Channelnomics sees these numbers more as directional indicators than guarantees. Our forecast for channel growth in 2025 remains positive — though more likely in the 4% to 7% range.

Have more questions? Our analysts have answers. Send your inquiries to info@channelnomics.com. And check out other Ask Channelnomics installments in the Channelnomics Insights section.